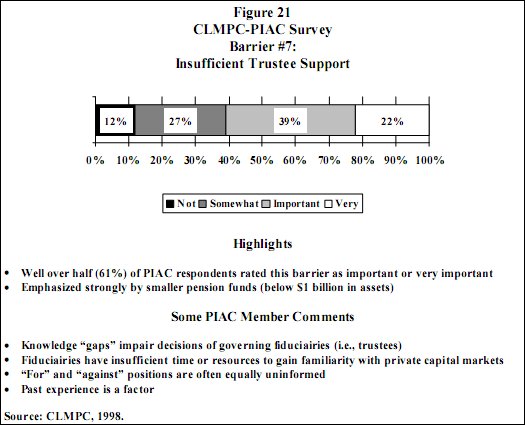

As the essential directive of Canadian legislative and regulatory frameworks, the prudent person rule emphasizes the process by which pension disbursements are made and not the specific capital markets in which they occur. As previously mentioned, this is also true in the United States and yet research there has shown that some pension fiduciaries still cite the law when electing to avoid certain high-risk private capital markets. Interestingly, this has happened even after American regulatory officials have published clarifications of legal parameters on this matter. This implies persistent gaps in knowledge. It also says a great deal about the understandable degree of caution exercised by fiduciaries because of their accountability under the law.

A total of 16 percent of PIAC respondents rated this barrier as important (12 percent) or very important (4 percent). Small and medium-sized pension funds gave it considerably more emphasis (50 percent important/very important).

The vast majority of PIAC respondents indicated that they did not see the law or prudential regulation and supervision by government, regardless of the jurisdiction, as a primary impediment. Some argued that if a violation took place, it would pertain only to injunctions contained in trustee-determined investment policies against allocations to such alternative/non-traditional asset classes.

This said, some respondents said that further and more explicit clarification of statutory requirements by Canadian regulatory authorities in federal and provincial jurisdictions is probably in order to dispel up any existing or future misconceptions in the minds of pension fiduciaries. Ideally, educational programs should also deal with these when focussing on the legal roles and responsibilities of trustees. This proposal is certainly consistent with the broad approach to pension governance recommended by PIACs 1997 guidelines (see Investing and Managing Pension Assets in Canada).