There has been, for example, gradual movement of large public sector pension plans away from a pattern of investing in non-marketable securities to first-time capital market participation. This is well illustrated by the recent history of the Ontario Teachers Pension Plan Board (PPB) which in 1990 had a $16 billion portfolio of non-marketable provincial bonds. In a few short years, it emerged with a portfolio that is broadly diversified by asset class, completely revamped according to its debt-equity ratio, and reaches into many capital markets, private and public, at-home and abroad. British Columbia public sector funds went through a similar transformation beginning in 1991. A parallel trend is the breaking-up of several massive public sector pools, sometimes precipitated by government privatization as happened in the case of the federal Transport Canada employees, or the spin-off fund from $100-plus billion superannuation account of the federal public service, scheduled to take effect in 2000.

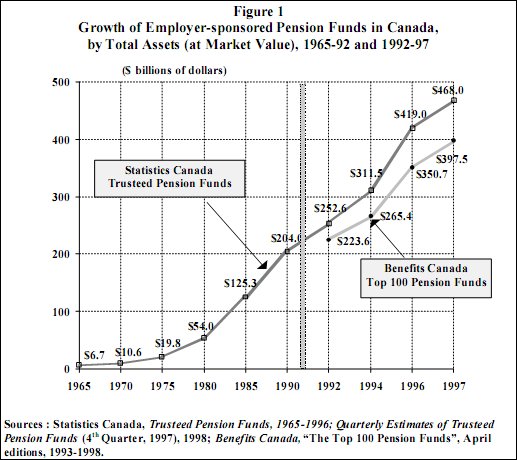

The cumulative result of these and other events has been a better than doubling of assets held by trusted pension funds from $204 billion at the beginning of the decade to $468 billion at the end of 1997 (see Figure 1). By mid-1998, total assets shot past the $500 billion level.

As Figure 2 shows, with assets of almost $53 billion at the end of last year, Ontario Teachers PPB is now Canadas largest individual pension fund, as it has been since 1993, followed closely at $49 billion by the Government and Public Employees Retirement Plan of Quebec. At nearly $30 billion in total assets, the third largest is the Ontario Municipal Employees Retirement System (OMERS). These three head Benefits Canadas list of the top 100 pension funds by exceptionally wide margins, given that the fourth largest the Hospitals of Ontario Pension Plan (HOOPP) stands at just over $13 billion.