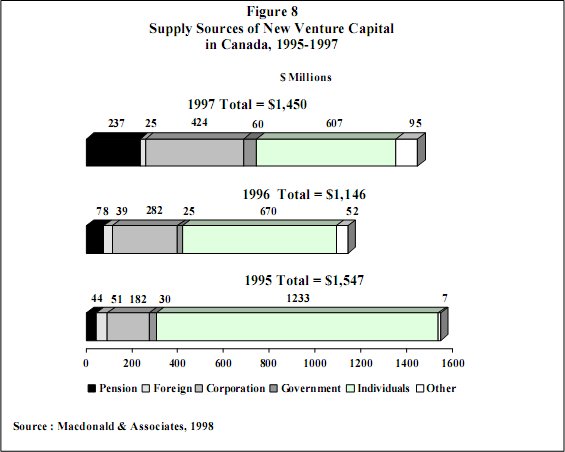

Using the database of Macdonald & Associates going back to 1985, the CLMPC estimates that current Canadian pension supply to the venture capital market totals approximately $800 million to $1 billion (or roughly 0.2 percent of total pension assets).

In practice, pension funds, both large and small, can participate in venture investing either directly, by co- investment with other financial institutions and pools often on an individual project basis and indirectly. Generally speaking, the indirect approach entails syndication of pension assets in a pooling vehicle situated externally, such as a limited partnership.

As mentioned earlier, indirect pension involvement through externally managed pooling and intermediation of the venture capital market is the most commonly-observed model. The most pervasive of all, the limited partnership, has demonstrated particular efficiency. This is because it allows pension funds and other institutional investors of all sizes to share the costs and risks of sometimes very small deals and sums and to defer the management-intensive tasks of finding, selecting, structuring and monitoring these deals to specialists. Given the finite supply of the latter with sufficient professional expertise to add investment value, pooling also permits multiple pension funds to take advantage of those available. For further discussion of this matter, see Of Pools and Pooling.

Both direct and indirect systems are in evidence in Canada. The following is an illustration of these, with particular reference to the return of pension funds to venture investing in 1997 or to activity that has been sustained without interruption since the 1980s, most prominently in Quebec.