Using data supplied by individual pension funds and Macdonald & Associates, the CLMPC estimates pension supply to private debt and equity investments in the Canadian middle market to have approximated $4-5 billion, at a minimum, in 1998 (or roughly 1.0 percent of total pension assets). Without knowledge of the current size of the market universe, it is not possible to say what proportion of total supply this represents. What is clear from CLMPC interviews with pension managers is that the share of total capital under management originating with large public sector funds has been on the rise since early in the present decade.Endnote 68

Pension funds can participate in the middle market either directly, by co-investment with other merchant banks, et al - often on an individual project basis - and indirectly. Generally speaking, the indirect approach entails syndication of pension assets in an externally-managed pooling vehicle, such as a limited partnership.

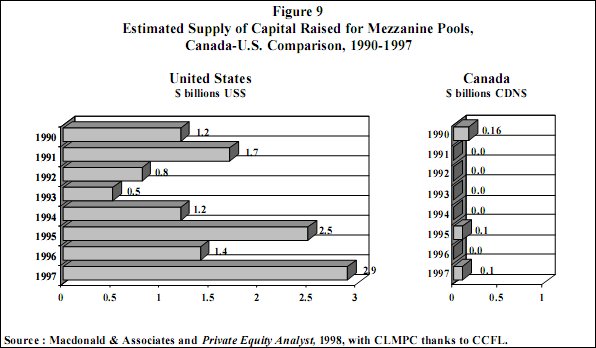

Due to its size, there are, in proportional terms, fewer limited partnerships and other pools in the Canadian market as compared to the United States (see Of Pools and Pooling. At present, costs and risks can be practically shared among a small group of merchant banks (both domestic and international), such as CIBC Wood Gundy Capital, Royal Bank Equity Partners and TD Capital Group and advisers/agents, along with the management-intensive tasks of finding, selecting, structuring and monitoring deals. This said, those pools that do exist (see below) are central to on-going investment activity. Room for this model may also grow in the years ahead, parallel to heightened demand and supply in the Canadian middle market.

A selection of direct and indirect systems in Canada is illustrated here.