Other PIAC respondents to the survey disagreed with the above perceptions, observing that so long as overall financial returns remained sound, bad publicity is always short-term and manageable through effective communications strategies. Some saw this as an acceptable cost of pension investment activity in private capital markets.

The 1996 Mercer study, Key Terms and Conditions of Private Equity Investing, commissioned by American pension funds, discussed at length the complex matters of recourse over outstanding liabilities and negotiations over limited partnership terminations, terminations of specific managers, liquidations and wind-downs (for details, see Of Pools and Pooling). Among other things, his study emphasizes the necessity of anticipating conflict scenarios and putting protections into partnership agreements for pension suppliers. When conflict provisions are triggered, or the agreement itself is transgressed, fiduciaries should have a range of allowable actions they can take, from discontinuing capital commitments to removing members of management teams or terminating altogether. Mercer also urges a highly methodical process for concluding pools and distributing proceeds.Endnote 144

As with other "best practices" in the United States, these may prove instructive to Canadian pension fiduciaries.

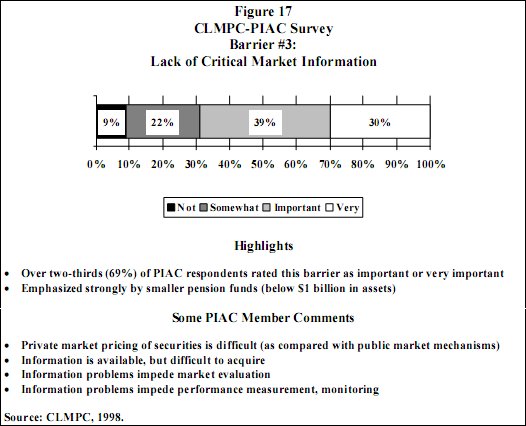

As stated above, governing and managing fiduciaries are hungry for information with which to assess, monitor and report on financial performance of a given asset class. Pension oversight procedures are, however, geared to conventional averages and indices for publicly-traded securities and market benchmarks that may be consulted quarterly, monthly, weekly or daily. When under-performance is clearly evident, these relatively liquid assets can be deserted or re-balanced within overall asset mixes. Illiquid investing in private capital markets cannot be judged or handled in this fashion. Deals involving private debt, equity and quasi- equity can endure up to ten years or more before exits and performance data may be unavailable or difficult to study closely in the short-term. Hence, the process of valuation is more complex.