Along with the prudent person rule, Canadian regulatory regimes spell out supplementary requirements of pension investment activity. For purposes of diversification, no more than 10 percent of a fund may be at risk in the assets of any one company or person. Neither may a pension fund own more than 30 percent of the voting shares of any one corporate entity. Foreign security holdings in a portfolio are also limited by the law, currently at a level of 20 percent. Among other strictures are those that cover investing in specific asset classes (e.g., real estate).Endnote 24

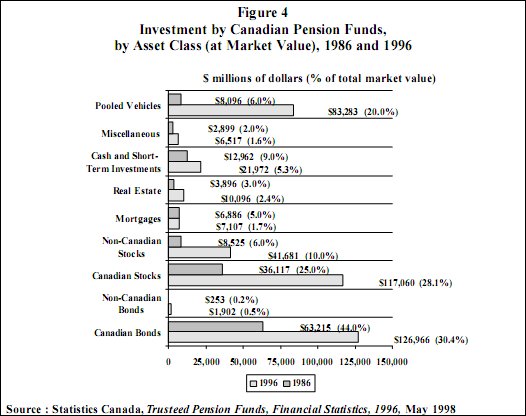

There appears to be a consensus among Canadian pension fiduciaries and experts that the original decision rendered by trustees about which asset classes best suit the investment policy of a given plan is by far the most vital. From this decision, flow all subsequent decisions concerning investment strategy.Endnote 25 All pension funds tend to favour investing in similar core asset classes, such as stocks and fixed income, and similarly project and gauge performance according to established market benchmark averages and indices (e.g., the TSE 300, the Scotia McLeod Universe Bond Index). There are, however, different strategic routes to obtaining capital appreciation and returns. There are, for instance, active and passive styles to approaching asset management.Endnote 26

Active management refers to pension investing that seeks to beat financial benchmarks by "picking winners." Tactically, this involves fiduciaries diversifying widely, trying to correctly read intelligence in a given capital market and being prepared to re-align portfolio exposure to assets when trends suggest new earnings potential. Passive management refers to pension investing in pools that replicate a stock or bond index or where portfolio exposure is otherwise geared to reflect a specified benchmark.