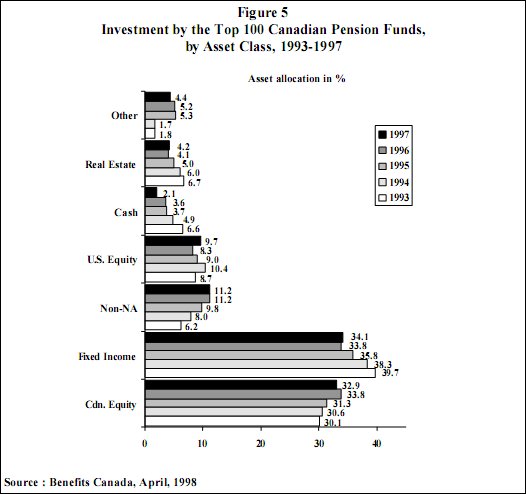

At the end of 1997, Benefits Canada estimates that just over $1.5 billion in assets of the largest Canadian pension funds flowed to venture capital and other forms of private debt and equity placement. Of course, this represents less than a fraction of one percent of the total for that year. As Figure 5 shows, real estate captured 4.2 percent of the total in this same category of funds. Not completely captured in this or Statistics Canada survey data is a modest upswing in pension asset allocations to these alternative/non-traditional asset classes, beginning in small increments in 1997 or one or two years earlier.Endnote 33

What is the connection between current patterns in pension asset allocations and change taking place in the Canadian economy? Of course, this is a big and multi-faceted topic that should be discussed with careful rumination about the numerous avenues by which pension investing in capital markets ultimately intersects with economic developments over long periods. However, the following may be regarded as something of an introduction to this much more expansive debate.

As indicated in the data of Statistics Canada and Benefits Canada, pension funds are pre-eminently creatures native to public securities exchanges. In the immediate past, when funds expressed their strongest predilection for fixed income assets, a role was carved out for them in the public market for corporate bond issues. Exponential growth in pools of pension capital in the late 1980s and the early 1990s was accompanied by exponential growth in this capital's exposure to corporate equity issues. This critical shift in the bond- to-equity ratios of funds has given them an unprecedented position both as institutional lenders and as institutional equity investors in exchanges.